If you’ve been keeping an eye on the news lately, you’ve likely noticed that the world feels a bit "heavy." While we usually try to keep our focus on the beauty of the islands and the strength of our local community, the reality is that what happens across the ocean eventually washes up on our shores. This week, that reality arrived in the form of a sharp uptick in mortgage rates.

After a relatively hopeful start to 2026, the recent escalation of conflict in Iran has sent ripples through the global economy. For those of us here on O‘ahu, where every percentage point can make a massive difference in a monthly mortgage payment, the latest data is something we need to talk about over some coffee (or a cold li hing mui drink).

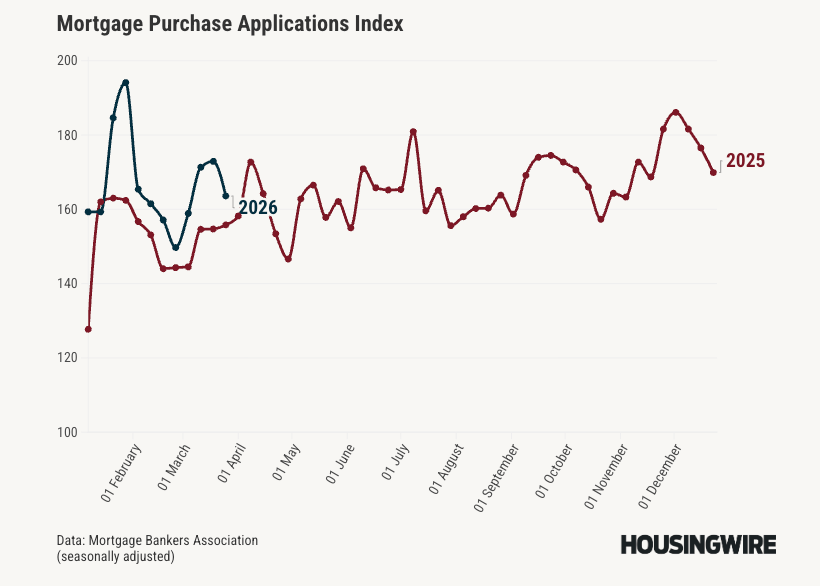

The National Picture: A Sudden Shift

For the first few months of this year, things were actually looking up. We had a softer labor market—with the last jobs report actually showing a loss of 100,000 jobs—and a general feeling that rates might stay lower for longer. Some buyers were even seeing rates dip below 6% before the conflict began. It felt like the "logjam" in the housing market was finally starting to loosen.

Then, things changed quickly. As conflict escalated, oil prices jumped and the 10-year Treasury yield—which mortgage rates love to follow—made a significant move higher following updates from the President that didn't suggest a quick fix. As of late March 2026, mortgage rates have spiked to approximately 6.62%, moving much closer to that 7% mark than the 6% we were hoping for.

Nationally, we’re already seeing the "brakes" being applied. Purchase applications, which were on a roll for most of the year, just took a 5% weekly dip. It’s a frustrating turn of events for anyone who was just about to pull the trigger on a new home.

Bringing it Home: The O‘ahu Impact

So, what does this mean for us in the 808? As we know, O‘ahu isn't the mainland. We deal with limited inventory, high demand, and price points that would make a Kansas resident faint. When rates jump like this, it hits our local families in a few specific ways:

- The "Wait and See" Game: In neighborhoods like ʻEwa Beach or Kapolei, where many first-time buyers look for single-family homes, a jump toward 7% can add hundreds of dollars to a monthly payment. We might see some local buyers pause their search to see if things settle down.

-

Condo Considerations: Over in Kakaʻako and Ala Moana, the "new era" of condo living is already facing pressure from rising insurance costs. Combine higher insurance premiums with higher mortgage rates, and the math for that two-bedroom suddenly looks a lot different.

- Inventory Stagnation: Many O‘ahu homeowners are currently sitting on "golden handcuffs"—mortgage rates from a few years ago that are 3% or lower. When market rates climb, these owners are even less likely to sell and trade up, because they don't want to lose that low payment. This keeps our inventory tight and keeps prices from dropping significantly, even if demand cools.

Is it all Gloom and Doom?

Not necessarily. While the volatility is frustrating, it’s important to remember that the O‘ahu market has always been resilient. We aren't like some mainland markets that see massive crashes; our land is finite, and people will always want to live in Hawai‘i.

The early part of 2026 showed us that there is a lot of "pent-up" demand. Housing demand was running smoothly and hitting multi-year highs in purchase applications before the war headlines hit. If the geopolitical situation stabilizes and rates find a steady floor—even if that floor is in the mid-6% range—buyers will eventually adjust their expectations and move forward.

Moving Forward with Perspective

It’s easy to get caught up in the headlines and the "what ifs." But for those of us living the island life, we know that things always cycle. If you’re a buyer, now is the time to be extra diligent with your "pencil sharpening." Work closely with a local lender who understands the nuances of the Hawai‘i market—someone who can help you look at buy-down options or specific programs that might take the sting out of these higher rates.

For sellers, it means your home needs to be "cherry." With rates higher, buyers are going to be more selective. They’ll want a home that is move-in ready, especially if they are stretching their budget to cover the higher interest cost.

We’ll keep an eye on the 10-year yield and the headlines for you. In the meantime, take a breath, enjoy the sunset, and remember that home is about more than just a percentage point—though we’d certainly like that point to be a little lower.

-Daniel Ulu